A Way to Ensure Retirement

by Patrick Egan

A mandatory savings plan may be the only way to ensure that everyone prepares for retirement.

Unions once exerted savings discipline for their workers by negotiating defined-benefit pensions, notes Teresa Ghilarducci, an economist at the New School for Social Research in New York. But such plans are becoming extinct, as employers shift the responsibilities and costs of retirement to employees via such defined-contribution pensions as the 401(k).

The problem? “Employers stop contributions whenever they’re in trouble or whenever they want to,” says Ghilarducci. “And employees often stop their contributions or cut them back.” Less than half of workers eligible for a 401(k) or similar plan actually contribute. So Ghilarducci has proposed guaranteed retirement accounts.

Though the recession has induced Americans to stop spending and start saving again, ending a two-decade slide in the personal savings rate, the long-term effects of the country’s collective shopping spree will become evident as baby boomers begin retiring. When they entered the workforce, their employers largely shouldered responsibility for funding their retirement; now, that burden rests with employees themselves, and too many have ignored the task.

“We run a real danger,” says David John, who researches retirement security at the Heritage Foundation, “that they get to a certain age and look in the money pot and there’s nothing there but a dead moth.” In fact, nearly a third of people 55 or older have $10,000 or less saved for retirement, according to an Employee Benefit Research Institute survey.

Another 20 percent have less than $50,000. Yet, those amounts, coupled with Social Security, are supposed to finance retirements that are lengthening along with life spans.

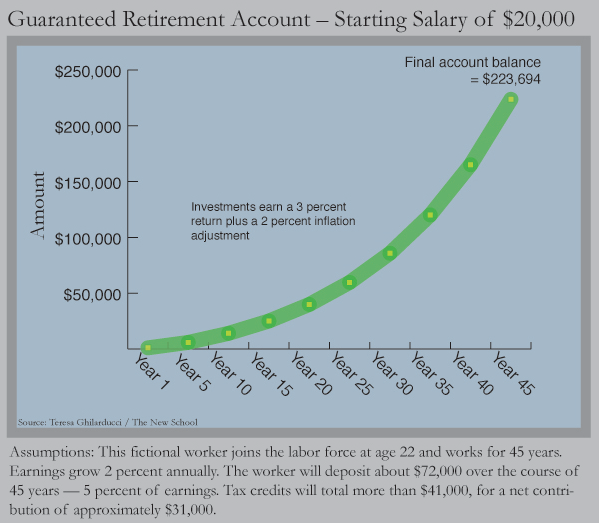

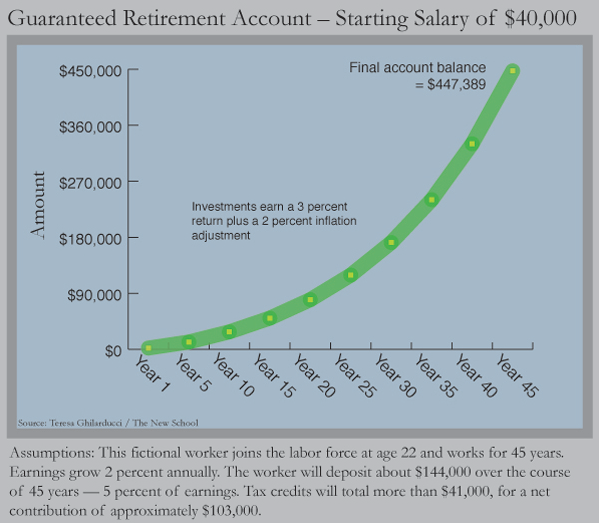

Ghilarducci’s guaranteed retirement account mandates that a minimum five percent of a person’s wages be deposited into a private account. All participants would pocket a $600 tax credit, offsetting the payroll reductions for lower earners.

Guaranteed retirement account projections

Guaranteed retirement account projectionsThose accounts would be far more stable than current IRAs, with a government-appointed board directing investments conservatively. The federal government would guarantee an annual 3 percent return—feasible, Ghilarducci says, because that’s roughly equal to the economy’s historic growth rate. If the assets earned more in a particular year, the government would reserve the surplus for leaner times. People won’t get rich through this plan, Ghilarducci cautions, but they will build more secure retirements.

To pay for the plan, Ghilarducci suggests abolishing tax benefits for the 401(k) system; it’s regressive, with about 70 percent of the benefit flowing to the top 20 percent of earners, according to the Urban Institute.

The question is whether Americans will agree to hand over more money to any government entity, even for their own eventual benefit. “Making wholesale revolutionary change is very difficult,” says John, of the Heritage Foundation. Ghilarducci’s system might’ve been welcomed at the height of the financial crisis, when trillions in retirement savings were wiped away. Now, he doubts it.

But voter sentiment doesn’t remain static. “If the great recession lasts as long as the pessimists think, the environment on this may change,” says Richard Leone, an economist and president of the Century Foundation. “Something’s got to give.”

The best repair may be one we impose.

-

A Doctor in the House

By reviving a practice from the past — house calls — the health care industry may be able to slash costs even as doctors give greater attention to older patients.

-

From Hospital Halls to Cyberspace

Telemedicine or e-care—technologies including remote patient-monitoring or videoconferencing—may prevent costly emergency room visits, hospital stays and nursing home use.

-

Rethinking Retirement

For millions of aging workers, the retirement age is sliding further away. Some will have to keep working; others will want to. Analysts ponder ways to make added work years viable and rewarding

-

Curing an Ailing Workforce

The health care industry needs millions of additional professionals with better geriatric skills to treat a surging older population. Two innovations are making headway.

-

Finding a Home to Grow Old In

Seniors want to age in place, but most will eventually require care. New senior housing options mix independent living with services as needed.

THIS PACKAGE IN DEPTH

To read about how this story came together and the reporters involved

Click Here.